Class 11 Business Studies Lesson 2 Notes

#Unit -2 Basic Issues of Economics

Factors of Production refers to those goods or services which are required to produce other goods and services. They are also known as inputs. Basically, there are four types of factors of production such as:

- Land

- Labour

- Capital

- Organization/Enterprise

1. Land

In narrow console, land is defined as the surface of the earth covered by soil. But in economic sense land refers to all the free gifts of nature to the living beings. It includes soil, forest, Himalaya, water, air, mines, sunlight etc. that is both on the surface and under the surface of the earth.

Features of land are:

Land is an important factor of production. It has some unique features which make land different from other factors of production. Some of them are discussed below:

1.1) Free gifts of nature

Land cannot be produced or created by man. It is given free of cost by nature. So, it does not hold any cost of production but it holds market value or price and its volume depends on its fertility or productivity.

1.2) Fixed in supply

Land is fixed in supply. Efforts of human beings cannot change its total size or amount. It cannot be extended or contracted by the will of humans.

1.3) Land is indestructible

Land is not destroyable. Human beings can destroy the quality of land but not the quantity. Fertility of land can be destroyed by efforts of humans or by other means. But the total size of land remains constant permanently.

1.4) Passive factor of production

Land is a passive factor of production. Human efforts are required to activate it to make land a productive factor. It means land alone cannot produce goods and services unless and until human efforts are made.

1.5) Immobile factor

Land is a fixed factor. It remains fixed where it is. Land is lumpy and indivisible in some cases. Since it is lumpy and indivisible, it is not transferable from one place to another.

2. Labour

Generally, labour is a physical or mental capacity of the human beings. But in economics, all the human efforts done mentally or physically with the aim of earning income is called labour. Thus, labour is the physical or mental effort of the human beings in the process of production.

Features of labour:

Labour is used to produce the goods and services through which he/she gets compensation in the form of wages. Some of the features of labour are explained below:

2.1) Labour is an active factor of production

Labour is the most active and indispensable factor of production. Generally, land and capital remain inactive and fruitless without the use of labour.

2.2) Labour is a perishable factor

Goods and services can be stored and sold in the future at high prices. But labour is perishable and cannot be stored like other factors. If it is not used or if the labourer doesn’t do a work, the labour is wasted and thus perishable.

2.3) Labour cannot be separable from labourious

Other factors of production like land and capital can be separated from their owner. But a labourious cannot separate his/her labour from themselves and send it to a different workplace. For eg. teachers cannot perform their teaching activities by sending their knowledge, organs of body and other teaching materials.

2.4) Labour is a mobile factor

Since land is immobile and capital is highly mobile, labour is a mobile factor. It can be transferred from one place to another. But it is less mobile than capital because it has a feeling of love and attachment with the family.

2.5) Refers in efficiency

Different labours have different degrees of working efficiency, working experience, skills, training etc. Due to having such different capacities, labour also gets different wages and salaries according to their contribution.

3. Capital

In general sense, capital is wealth or money. But in economic sense, it refers to all man-made artificial goods which are used for the further production of wealth. Machines, tools, buildings, roads, bridges, raw materials etc. are the examples of wealth.

Features

Some of the features of capital are as follows:

3.1) Man-made factor

Capital is not automatically created, but it is produced with human efforts as well as other means of production. For eg. land is not man-made but machines, vehicles, etc. are man-made factors of production. So, all capital is made by man.

3.2) Passive factor of production

Since it is produced by human beings, capital by itself remains unproductive if it is not used by human beings to produce wealth. Unless there is involvement of labour, machines do not give production.

3.3) Most mobile factor

Most capital can be transferred from one place to another or from one use to another. So it is taken as a mobile factor. Various forms of capital like machinery, money, equipment, vehicles etc. are mobile.

3.4) Supply of capital is elastic

Unlike land, the supply of capital is elastic. Its supply can be increased or decreased according to the need of the economy. For eg. the supply of tools, machinery, etc. can be increased or decreased as per society’s requirement.

3.5) It depends upon technology

The amount of capital depends upon the level of technology employed by a nation. The more progress there is in a country’s technology, the more capital is produced in that nation.

4. Organization or Enterprise

It is defined as the collective body of active human resources established for the utilization of factors of production like land, labour and capital in the line of production process. It also organizes and co-ordinates all the above factors of production to earn a profit. Some of the features are as follows:

4.1) Collection of people

An organization is established with the help of people. To achieve the goal and target of the organization, individuals are assigned different roles to accomplish various tasks.

4.2) Risk and uncertainty bearing

Risk and uncertainty is very important for an organization. There is the risk of loss due to uncertain future events such as natural calamity, change in fashion etc. So the organization should have the capacity to bear such unexpected conditions.

4.3) Profit motive

The main objective of an organization is to earn profit and to accumulate wealth. It is also essential for survival as well as expansion for further organization.

4.4) Environment

Organization operates in an open environment. It is affected by changes in external factors like political, economic, socio-cultural factors, etc.

4.5) Division of labour

Division of labour is very important for the organization to flourish. It is possible on the basis of potential training and skills of the labour in different units or departments.

Concept of Scarcity and Choices

Scarcity and choice are the basic problem in economics. This concept was developed by economists Lionel Robbins in 1932 AD. Human wants are unlimited but resources to meet them are limited which creates the problem in any economy and all as economic problem.

Concept of Scarcity

Scarcity refers to the condition of insufficiency where the human beings are incapable of fulfilling their desires in sufficient manner. In other words, the scarcity in economic sense is that the commodity becomes scarce to satisfy the desire of individuals, society, nation as well as entire world.

As the human wants are unlimited. We may satisfy some of our wants but soon new wants arises continuously with the multiplication. Thus, scarcity explains the relationship between unlimited wants and limited resources and the problem like poverty, inequality, unemployment and so on.

Concept of choice

Choice is the process of efficient selection of few goods or wants from the bundle of goods or wants. As the human beings are suffered from the lack of resources but they have to fulfill their unlimited demands, there is the problem of choice. So, they are unable to fulfill their unlimited desires. During the fulfillment of their unlimited desires, some desires should be sacrificed to satisfy some other desire. Hence the people postponed less urgent wants to satisfy the more urgent wants at first. for eg, if a boy has the desire of purchasing the economics book, he should sacrifice to visit cinema hall. Thus, economic problem because of unlimited wants and scarce resources is as shown below chart

Opportunity cost is defined as the second best alternative that has been sacrificed by the consumer or producer by taking an economic decision. In other words, it is also defined as the next best alternative that has been for gone. for eg, student has 3 hours time with him or her and there are two alternatives first is, completing the economic homework and second one is watching the movie in QfX Cinema hall. If a student decides to do homework its opportunity cost is the entertainment that could be received by watching movie. If he/she goes for movie it’s opportunity cost is doing his/her homework.

Allocation of resources

Allocation of resources means the scientific and appropriate management utilization of scarce resources in the production, distribution of exchange. It deals with how much of the resources in which and what sector. It is the basic problem of every because all of the economic have limited resources but unlimited desires and wants. The main objective of allocation of resource is to achieve the maximum satisfaction from the utilization of lack of resources. In order to allocate the resources the following problem should be considered:

1) What to produce?

This means what types of and what amounts of goods and services to produce by how much or in what quantities. Every wants of individual cannot be satisfied by the producers. So. the producer, society and even the nation must choose the best alternatives from above in order to satisfy the public desires in the market.

2) How to produce?

The second problem related to allocation of resources is concerned with the methods of production. It means either to use labour intensive technology or to use capital intensive technology. So, the decision should be made on the basis of his/her capacity or available resources.

3) Whom to produce?

Due to the Scarcity of resources the producer cannot satisfy all the wants of the consumers. So decision have to be taken concerning with how many of each wants are to be satisfied. For eg. whether the production is for teenager or for middle age group or for old age group. In this way the scarce resources should be allocated and should be decided whom to Produce goods and services.

4) Sector development?

While allocating the resources, nation should give equal priority for the balance development to all the sectors such as primary sector (agriculture), Secondary sector (Industry) and service sector (banking and official sector) of the whole economy.

Concept of Production Possibility Curve (PPC)

As the human wants are unlimited but resources to meet this wants are limited or scarce .This creates problem of choice and this problem can be explained graphically with the help of production possibility Curve.A production possibility refers to the alternative combination of goods and services that could be produce with all the available resources within a specific Period of time. The concept of PPC was developed by P.A. Samuel Son. According to him PPC is that curve which represents the maximum amount of pair of goods that can be both produced with in an economy by the available resources and technique.

In other words, It is the graphical representation of various combination of goods and services that an economy can produce with the full use of the given resources and state of technology.

ASSUMPTIONS

The concept of PPC is based on the following Assumptions:

1) Economy is producing only two goods.

2) There is full employment of resources.

3) Production technology is given and constant.

4) Factors of production are fixed.

5) Time period is given or it is for specific period.

6) The concept of PPC can be explained by the following table and graph

Here is the data you provided in proper table format, as per your guideline:

| Possibilities/Combinations | Consumer goods (000) | Capital goods (000) |

|---|---|---|

| A | 0 | 15 |

| B | 1 | 14 |

| C | 2 | 12 |

| D | 3 | 9 |

| E | 4 | 5 |

| F | 5 | 0 |

The above table shows that the producer can produce a maximum of consumer goods and no capital goods at the combination ‘F’. It is because of the scarcity of resources. In this way the producer select the different combinations like A, B, C, D, E for the production of consumer goods and capital goods.

The above table can be represented by the below graph.

In the above figure, the consumer goods and capital goods are measured along x-axis and y-axis respectively. Combination ‘A’ represents the production possibility of 15000 of capital goods and no consumer goods. Similarly, point B, C, D, E and F represents the different combinations of capital goods and consumer goods. So ‘A’ ,’F’ is a PPC.

In the figure, the point G represents that it is a inefficient point because the resources are not fully utilized. The point ‘H’ represent that it is unattainable point because the producer is suffered by scarcity of resources. Thus, the consumer has to choose the possible possibilities on the PPC in order to produce goods and services.

Goods & Services

Goods are all those tangible things on commodities that are used to satisfy human desires. In other words, all the commodities having utility are called goods. For eg foods, clothes, golds, silvers etc are the goods.

Services are the human works, efforts which are intangible but satisfy the human wants. For eg, doctor’s work, lawyer’s work, teacher’s work, performing musics & dances, etc are example of Services.

Types of goods:

1) Normal goods:

Those goods are normal goods whose quantity demanded increases as the income of the consumer increases and vice versa. It means there is the positive relationship between income of the consumers and demand of such goods. All the daily consumable goods are normal goods.

2) Inferior goods:

The goods are inferior goods whose quantity demanded increases with the decreasing income of the consumer and vice – versa. It means there is negative relationship between income of the consumer and quantity demand of such goods. For eg: Black & White Tv, Street food & clothes etc are inferior goods.

3) Giffen goods:

Giffen goods are special types of inferior whose quantity demanded increases with the increasing price and vice-versa. This types of goods are generally consumed by the poor people of remote areas. It was firstly developed by Economist Sir Robert Giffen. It has positive relationship between price of such goods and quantity demand.

4) Substitute goods:

The goods which partly or fully satisfy the same needs of consumers are called substitute goods. In other words, these are the goods which can be used in place of each other. For eg, tea & coffee, coke & Pepsi, jell pen & ink pen etc. In such goods, there is the positive relationship between price of the commodity and the quantity demand of its substitute.

5) Complementary goods.

The goods which are used together to satisfy a want is called complementary goods. In other Words, the goods which are useless in the absence of another is called complementary goods. For eg, Pen & ink, Shoes & shock, car & petrol etc. In such goods, there is the negative relationship between price of the commodity and quantity demand of its compliment.

6) Private goods

The goods which are produced by and owned by private individual or enterprises is called private goods. In other words, the private goods also defined as the goods having the features of rivalry and excludability.

7) Public goods

The goods which are owned by society and government and also common to all are called public goods. In other words, public goods are also defined as goods having the features of non-rivalry and non-excludability. For eg: roads, bridges, parks etc.

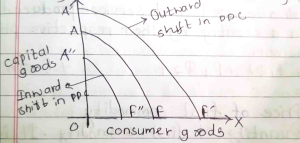

Shifts in PPC (Production Possibility Curve)

The movement of PPC from its initial position to inward (downwards) and outward (Upward) position due to the change in technology, capital, skill of labour, raw materials, etc is called shifts in PPC. Causes of outward Shift in PPC:

a) Due to improvement in productivity of labor through training & education

b) Due ta the availability of her raw materials in large quantity.

c) Due to technological progress.

d) Due to the available of natural materials (land) for the production in large quantity.

Causes of inward shift in PPC

a) Backwardness in technology

b) Shortage of natural resources

c) Lack of training & skill development programs to the labor

d) Decrease in involvement of capital, machinery and equipments.

e) Decrease in size of population due to war, emigration.

The shift in PPC can be shown by following graph:

In the above figure, the curve A F is the Initial PPC which is plotted due to the various combination of two goods and services produced by an economy or producer by the available resources & technology. If the resources as well as technology is positively change the original PPC shift towards right i.e. called outward shift which is denoted by A’ F’ curve. Similarly, if the resources and technology are negatively changed, the original PPC will shift towards left i.e. called inward shift which is denoted by A” F” in figure.

Concept of GDP, GNP

Gross Domestic Product (GDP) is defined as the total market value of all the final goods and services produced within a geographical boundary of country during a year. In other words, it is also calculated by muliplying all the goods and Services produced within a country by their respective price in a year.

GDP = P1Q1 + P2Q2 +…….PnQn

Where,

P1= Price of first commodity

Q1= Quantity of first commodity. It is equal to price of second commodity and so on.

Features of GDP

a) GDP is a market/money value of goods services

b) GDP includes only currently produced goods and services.

c) GDP includes goods and services produced with the country.

d) GDP includes only the money value of final goods.

e) It excludes transfer payment.

GNP

Gross National product (GNP) is defined as the market value of all the final goods and services produced during a year by domestically owned resources. In other words it is also defined as the total market value of all the final goods and services produced in a country + net factor income from abroad (NFIA)

GNP = GDP + NFIA

Features of GNP

a) GNP is a market/money value of goods and services.

b) GNP includes only currently produced goods and services.

c) GNP includes only the money value of final goods.

d) GNP includes goods and services with the country

e) It excludes transfer payment.